Regime shift: Investing in a new Fixed Income world

We believe this year's market environment will feature less central bank intervention, leading to more volatility than the prior decade. Increased volatility will cause more disruptions and dislocations - and more instances for a dynamic multi-sector manager to add value.

Authors

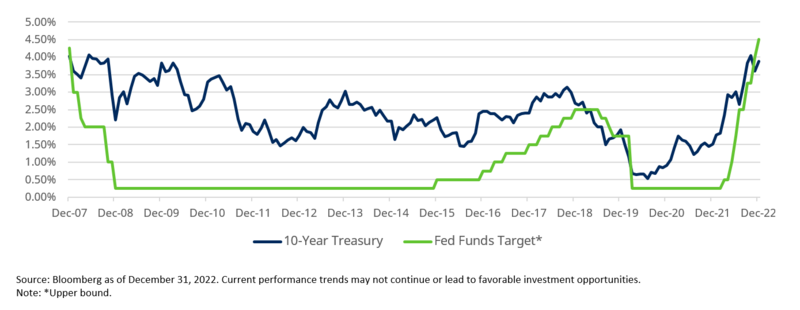

The rapid rise in Treasury yields this year has attracted the pen of many opinions and the resulting negative returns, the worst in over 200 years, have inspired even more debate. This unprecedented market move is now in the rearview mirror and it is time to assess today's fixed income landscape and outlook. It has been more than a decade since we have seen yields at this level and it has been some time since investors have considered Treasury bonds an attractive option for income (see Figure 1).

Figure 1: 10-Year Treasury yield vs. Federal Funds target rate*

There has been a significant regime shift at the Federal Reserve (“the Fed”) over the last nine months. The accommodative monetary policy that investors have come to expect since the Global Financial Crisis has ended as the Fed is now actively trying to temper growth to lower inflation – even if it means causing a recession. Over the last decade, The Fed has cut interest rates to record lows, which produced an environment that forced investors to accept more risk by moving down the credit spectrum, further out the yield curve or into less liquid assets to achieve their return targets.

The backdrop of fixed income looks much different today. Investors now can invest in higher quality parts of the market, like short duration investment grade corporates, Treasuries or agency backed mortgages, and earn attractive yields. In fact, those are the segments of the market that we believe are the most attractive as growth concerns and rising expectations of a recession overtake the focus of inflation that has persisted for the last 12-18 months.

It is important to note the global regime shift taking place today results from a significant change in both monetary and public policy. Low inflation, cheap/abundant labor and energy have bolstered the last few decades. These trends are changing and have structural implications for markets. A regime with higher input costs (whether due to labor or energy) means that inflation could run structurally higher, which will cause monetary policy to remain more hawkish and lead to shorter boom/bust cycles. This volatility and higher cost of capital will have a material impact on business investment and the allocation of resources.

We believe the market environment over the next year will feature less central bank intervention that will lead to more volatility than the prior decade. Increased volatility will cause more disruptions and dislocations and therefore more instances for a dynamic multi-sector manager to add value. Our value-driven philosophy combined with our opportunistic, high conviction approach lends itself to shift allocations towards pockets of promise. We are unbiased as to where those opportunities arise, whether it be it in agency mortgage backed securities, municipals or corporate bonds. We will deploy capital wherever we see the most attractive relative value prospects. We possess a history of capitalizing on market dislocations and have been building liquidity across all of our strategies over the last several months. As the market morphs, we are ready to adjust our allocations. We accept short-term volatility and instead focus on longer term value propositions, which are reflected in our attractive performance over the last three-, five- and ten-year timeframes.

In addition, while the majority of managers are positioned to short index duration, our benchmark-aware methods have always maintained a neutral stance on duration. Our focus is to add alpha through our ability to identify the inflection points in markets and to allocate capital to those undervalued sectors and issuers. We have demonstrated an ability to do this successfully during various periods of volatility. The following (see Figure 2) are a few examples: Taper Tantrum (2013), energy crisis (2015-2016) and most recently the pandemic (2020).

Figure 2: Core strategy allocation (in market value %) relative to the benchmark vs valuations

It is clear that the current environment and the Fed’s aggressive policy this year have led to a different market than the one we experienced this last decade. We believe investors should opt for a dynamic and active manager with proven credentials to capitalize on market dislocations during periods of elevated volatility. This could lead to outperformance over the coming years.

The views and opinions contained herein are those of Schroders US Multi-Sector Fixed Income team, and do not necessarily represent Schroder Investment Management North America Inc.’s house views. These views are subject to change.

All investments involve risks including the risk of possible loss of principal. The market value of the portfolio may decline as a result of a number of factors and may not return to the original amount invested. Investing in fixed income securities involves additional risk such as interest rate risk, credit risk, inflation/deflation risk, government securities risk, foreign investment risk, currency risk, derivatives risk, leverage risk and liquidity risk. Investing overseas involves special risks including among others, risks related to political or economic instability, foreign currency (such as exchange, valuation, and fluctuation) risk, market entry or exit restrictions, illiquidity and taxation risks. These risks exist to a greater extent in emerging markets.

The material is not intended to provide, and should not be relied on for accounting, legal or tax advice, or investment recommendations. Information herein has been obtained from sources we believe to be reliable, but Schroders Plc does not warrant its completeness or accuracy. No responsibility can be accepted for errors of facts obtained from third parties. Reliance should not be placed on the views and information in the document when taking individual investment and/or strategic decisions. The opinions stated in this document include some forecasted views. We believe that we are basing our expectations and beliefs on reasonable assumptions within the bounds of what we currently know. However, there is no guarantee that any forecasts or opinions will be realized. This document does not constitute an offer to sell or any solicitation of any offer to buy securities or any other instrument described in this document. Past performance is no guarantee of future results.

Schroder Investment Management North America Inc. (“SIMNA Inc.”) is registered as an investment adviser with the US Securities and Exchange Commission and as a Portfolio Manager with the securities regulatory authorities in Alberta, British Columbia, Manitoba, Nova Scotia, Ontario, Quebec and Saskatchewan. It provides asset management products and services to clients in the United States and Canada. Schroder Fund Advisors LLC (“SFA”) markets certain investment vehicles for which SIMNA Inc. is an investment adviser. SFA is a wholly-owned subsidiary of SIMNA Inc. and is registered as a limited purpose broker-dealer with the Financial Industry Regulatory Authority and as an Exempt Market Dealer with the securities regulatory authorities in Alberta, British Columbia, Manitoba, New Brunswick, Newfoundland and Labrador, Nova Scotia, Ontario, Quebec, and Saskatchewan. This document does not purport to provide investment advice and the information contained in this material is for informational purposes and not to engage in trading activities. It does not purport to describe the business or affairs of any issuer and is not being provided for delivery to or review by any prospective purchaser so as to assist the prospective purchaser to make an investment decision in respect of securities being sold in a distribution. SIMNA Inc. and SFA are wholly-owned subsidiaries of Schroders plc, a UK public company with shares listed on the London Stock Exchange. Further information about Schroders can be found at www.schroders.com/us or www.schroders.com/ca. Schroder Investment Management North America Inc., 7 Bryant Park, New York, NY 10018-3706, (212) 641-3800.

Important Information: This communication is marketing material. The views and opinions contained herein are those of the author(s) on this page, and may not necessarily represent views expressed or reflected in other Schroders communications, strategies or funds. This material is intended to be for information purposes only and is not intended as promotional material in any respect. The material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. It is not intended to provide and should not be relied on for accounting, legal or tax advice, or investment recommendations. Reliance should not be placed on the views and information in this document when taking individual investment and/or strategic decisions. Past performance is not a reliable indicator of future results. The value of an investment can go down as well as up and is not guaranteed. All investments involve risks including the risk of possible loss of principal. Information herein is believed to be reliable but Schroders does not warrant its completeness or accuracy. Some information quoted was obtained from external sources we consider to be reliable. No responsibility can be accepted for errors of fact obtained from third parties, and this data may change with market conditions. This does not exclude any duty or liability that Schroders has to its customers under any regulatory system. Regions/ sectors shown for illustrative purposes only and should not be viewed as a recommendation to buy/sell. The opinions in this material include some forecasted views. We believe we are basing our expectations and beliefs on reasonable assumptions within the bounds of what we currently know. However, there is no guarantee than any forecasts or opinions will be realised. These views and opinions may change. The content is issued by Schroder Investment Management Limited, 1 London Wall Place, London EC2Y 5AU. Registered No. 1893220 England. Authorised and regulated by the Financial Conduct Authority.

Authors

Topics