Geopolitical concerns and fears of a global economic slowdown have soared as investors increasingly embrace private assets, Schroders Institutional Investor Study 2019 has found.

The study - which surveyed 650 institutional investors encompassing approximately $25.4 trillion in assets – has identified a growing apprehension among investors amid a backdrop of increasing macroeconomic uncertainty.

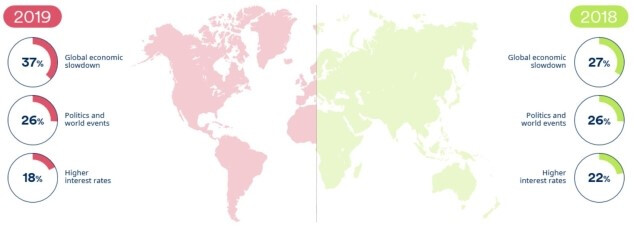

More than half of investors (52%) said that politics and world events such as Brexit and trade wars would impact portfolio performance over the next 12 months. This is a marked increase on 32% of investors in 2017 and 44% in 2018.

Over a third of investors (37%) also cited a global economic slowdown as the biggest concern, significantly up on 27% a year ago. These findings are perhaps reflective of the continued trade dispute between China and the US, as well as the growing uncertainty ahead of the Brexit deadline.

What influences worry you the most?

Higher interest rates were cited as the biggest influence on portfolio performance, although this was to a lesser extent than a year ago. In contrast, factors previously thought to be very influential – such as monetary policy tapering, regulation and the risk of cyber-attacks – have all steadily decreased in importance over the past 12 months.

In terms of asset classes, appetite for emerging markets (EMs) has fallen among institutional investors, with allocations dropping from 15% in 2017 to 10% this year. Expected allocations towards EMs over the next 12 months have also slipped to 9%.

Just a third of investors (29%) are holding their investments for 3-5 years, with only 10% remaining invested for a full cycle. This comes as more than half (53%) of investors stated there is a greater need for customized or bespoke products because off-the-shelf funds are failing to meet their organization’s financial objectives.

Focus on private assets

Driving investors’ returns expectations is their continuing focus on private assets. More than half (52%) expect to raise their allocations to private assets over the next three years. Investors in North America (58%) and Asia (50%) were the most intent on doing so.

Investors globally cited the need to generate higher returns and portfolio diversification as the two biggest factors encouraging them to invest in private assets.

Across the private asset spectrum, private equity was viewed as the source of greatest potential returns, with 69% of investors anticipating returns of over 5%. Further supporting this view, out of the main private assets classes, 37% of investors globally are intending to increase their allocations to private equity, markedly ahead of private debt, infrastructure equity and real estate.

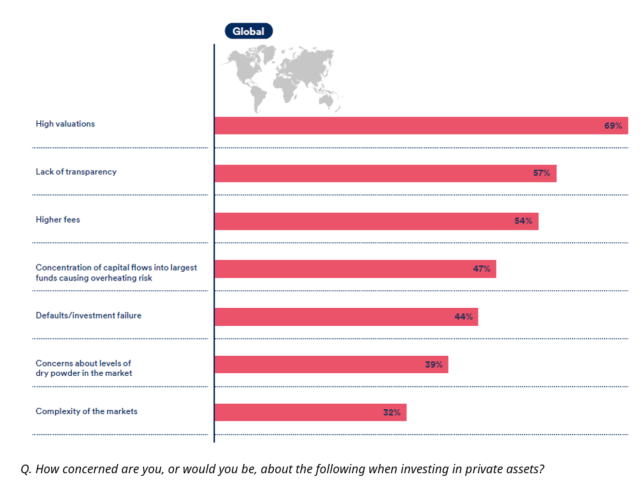

Investors however cited the cost and complexity of fees as the greatest challenge to investing in private assets, and also flagged high valuations as the primary concern when investing in the asset class.

Overall return expectations

Despite these macroeconomic pressures, investors’ return expectations have, however, remained steady over the past 12 months. The majority of investors globally (57%) are factoring in annual returns of 5%-9% annualized over the next five years. This compares to 60% of investors a year ago.

Geographically, the gap between a bullish North America and more cautious investors in Europe has significantly widened.

Over three-quarters (77%) of North American investors are estimating returns of 5%-9%, a marked difference to 42% of investors in Europe.

Charles Prideaux, Global Head of Investment, Schroders, commented:

“Institutional investors can be forgiven for beginning to fear the worst. A number of geopolitical uncertainties have been hanging over their heads for some time now and it currently is impossible to say if there is any sign of these concerns abating.

“It is encouraging to see that despite these challenges, investors’ return expectations – with the exception of those in Europe – remain relatively robust and their holdings periods are remaining stable. Chopping and changing investments, particularly during challenging times, is likely to be detrimental for investors’ portfolios and could lead to disappointing investment returns.

“It is incumbent on the likes of Schroders to work in partnership with institutional investors to help them navigate this uncertainty and deliver investment solutions which meet their investment objectives and risk appetites.”

Georg Wunderlin, Global Head of Private Assets, Schroders, commented:

“Institutional investors are increasingly aware that they can afford a higher share of illiquid assets in their portfolios, given their long-duration liabilities. They are therefore looking to capture the illiquidity premium while adding diversification to their portfolios.

“Private assets offer a broad investment universe with a wide range of risk and return, correlation, cash-flow, and risk capital characteristics. Private assets portfolios can be tailored to deliver the outcomes needed for each specific investor.

“In the current market environment investors are particularly interested in strategies based on ‘deep operational skills’ where performance can effectively be ‘manufactured’ by the responsible investment teams. Examples are small and midcap buyouts in private equity or differentiated value-add strategies in real estate. In these areas investment performance is considerably less influenced by market cycles.”

This global study was commissioned by Schroders for the third consecutive year to analyze institutional investors and their attitudes towards investment objectives, risks, private assets and sustainable investments.

The respondent pool represents a spectrum of institutions, including pension funds, insurance companies, sovereign wealth funds, endowments and foundations managing approximately $25.4 trillion in assets.

The research was carried out via an extensive global survey during May 2019. The 650 institutional respondents were split as follows: 175 in North America, 250 in Europe, 175 in Asia and 50 in Latin America.

Respondents were sourced from 20 different locations across the world.

For further information, please contact:

Katherine Segura of Prosek Partners at 646-818-9266, ksegura@prosek.com

Jennifer Manser O’Rourke of Schroders at 212-632-2947, jennifer.manser@schroders.com

Important information

The views and opinions contained herein are those of Schroders’ investment teams and/or Economics Group, and do not necessarily represent Schroder Investment Management North America Inc.’s house views. These views are subject to change. This information is intended to be for information purposes only and it is not intended as promotional material in any respect.