Schroders Institutional Investor Study: optimism surges for investment returns

Institutional investors are expecting an improvement in returns despite the long-lasting challenges created by the Covid-19 pandemic.

Authors

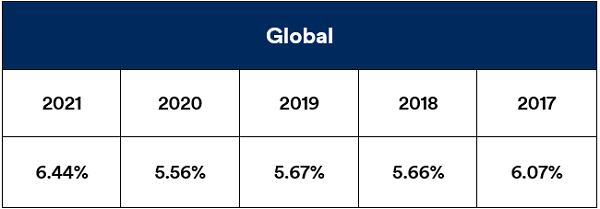

The annual Schroders Institutional Investor Study, which polls 750 industry professionals in 26 locations across the globe, showed an average expectation return of 6.4%, up from 5.6% a year earlier.

Almost half of respondents estimate that their average annual total return will be above 6% over the next five years, with 13% expecting returns of more than 9%.

These expectations are higher than last year, when only 35% of global investors thought they could return over 6% and 5% believed they could top 9%.

Keith Wade, Chief Economist, said: “Clearly, confidence is rising. This is due to a combination of vaccine success, increasing consumer demand across the globe, and indications that the global economic recovery from Covid-19 could be relatively swift.

“However, expectations are even higher than before the pandemic hit, indicating a more sustained shift in confidence. It could be that even professional investors are being swayed by the strong real returns achieved by both equity and bonds in the past decade. Understandably, they’re feeling more optimistic. The reality is that, to achieve decent returns, investors will need to navigate a number of challenges, from low rates to demographic shifts to technological disruption.

“To survive, investors should be considering whether to invest by theme – to capture the growth from global super trends – or perhaps whether they should diversify into fast-growing areas of private assets, such as private equity, infrastructure debt or real estate.”

A global return to confidence

Expectation of high returns has improved across all regions, the study reveals, but sentiment in certain parts of the globe is particularly striking.

In Latin America, institutional investors have changed their projections dramatically since last year. Just over half (54%) expect their annual return to be above 6% for the next five years, compared with 28% last year.

In North America, 45% were expecting returns of 6% or above in 2020, and 7% were expecting above 9%. That has now increased to 54% and 11%, respectively, making institutional investors in the region the most bullish in the world on returns.

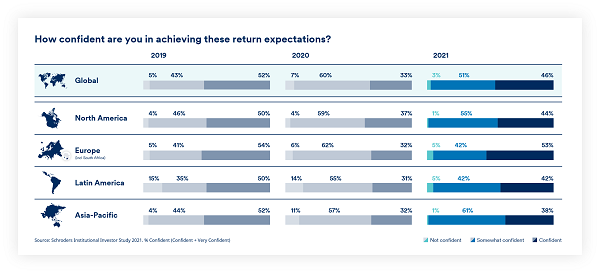

All regions also showed a marked increase in confidence in their predictions compared with last year, indicating that they are expecting fewer “curve balls” from the pandemic in the coming months.

Overall, 46% of institutional investors said they were “confident" that they would meet their return expectations, compared with 33% in 2020.

However, confidence has not yet rebounded to pre-Covid-19 levels, suggesting that there is still residual concern about the fragility of global recovery. In 2019, 52% of respondents were confident about meeting their expectations, while the figure was 51% the year before.

Investors in Asia-Pacific have the lowest confidence in their expectations, with 38% saying they are confident, 61% somewhat confident and 1% not confident at all.

That compares with Europe, where 53% of institutions are confident of returns, up from 32% last year but slightly down from their position in 2019.

Only one in six respondents said they were lowering their return target, despite continued low rates, with 53% keeping it the same.

Meanwhile, despite a slight increase in emerging markets allocation, and a small downward trend in allocation to private assets, portfolio allocations and expected allocations remain similar.

There may be changes in the pipeline though, with over half (53%) stating they will review their entire investment strategy in the coming year to ensure that it is still current.

Keith Wade said: “The pandemic is still seen as having the biggest influence on portfolio performance, but has fallen significantly compared to a year ago, along with the effect of the global economic slowdown. The improvement in global growth prospects is clearly having an influence here and investors are beginning to get concerned about a withdrawal of liquidity through a tapering of monetary policy. Overall, though, negative or ultra-low interest rates are seen as a highly significant influence on portfolios.”

Climate risk moves into the frame as Covid-19 anxiety fades

While anxiety around the impact of Covid-19 is fading, it is being replaced with other concerns, including an increased focus on climate risk.

Although the pandemic and global economic slowdown are still seen as the primary factors influencing investment performance overall, fewer respondents now feel this way. Compared to 2020, 61% are now primarily concerned with the pandemic, down nine percentage points, and 58% are concerned with global slowdown, down 21 percentage points.

Concern around climate change risk, in contrast, has risen sharply. Where 8% saw this as a primary factor influencing investment last year, that percentage has now risen to 21%.

Irene Lauro, Economist, has examined the impact climate change might have on markets. She said: “Climate change poses significant risks to the global economy and investment portfolios, as we highlight in our analysis on physical and transition costs and stranded assets. Climate change is also likely to be an investment opportunity as it creates winners and losers. The financial sector has a key role in supporting sustainability as institutional investors can help build environmental resilience by decarbonising their portfolios and redirecting investments to solutions to tackle climate change.”

With many of us working at home, and businesses concerned about the security of their remote working strategies, more investors than ever are also worried about the investment risks from cyber attacks. Just 5% listed this as a primary concern in 2020. That is now up to 12%.

ESG: still complex but now more important

With climate change high on the risk agenda, institutions of all types are keen to focus on sustainable investment. However, the study shows that many are finding this a complex and difficult area to get right.

The majority of institutional investors describe ESG investing as “somewhat challenging” or “very challenging”. Last year, 55% described it as somewhat challenging, and this has risen to 63%, while the percentage describing it as very challenging has risen from 15% to 17%.

More than half of institutional investors think ESG is more important because of Covid-19. This is particularly the case among European investors – 62% of them now attach a greater significance to ESG. North America is an outlier in this respect, with 52% stating that the pandemic has had no impact on the importance of ESG investing, while 7% feel it is less important.

Andy Howard, Global Head of Sustainable Investment, said: “The pandemic has impacted all aspects of our lives and sustainable investing is no exception. Covid-19 has sharpened investors’ focus on ensuring their assets are being directed in the most sustainable ways. The global economy has a long way to go to return to pre-pandemic levels but ensuring that the recovery is sustainable is a key objective for many now.

“As investors, there is clearly work that still needs to be done to support this change. We need to ensure that any concerns or challenges our clients may perceive when it comes to investing sustainably are completely allayed, through ever clearer reporting and disclosures.”

‘Greenwashing’ a major concern

Concerns around “greenwashing”, where investments are badged as green but are less sound on close investigation, are a major issue for institutional investors.

For the second consecutive year, greenwashing is cited as the most challenging issue investors face. Almost six in ten investors globally are worried by this due to a lack of clear, agreed definitions on what sustainable investment is.

Institutions are now far less concerned about whether their ESG funds will underperform. While 51% were concerned about performance in this sector in 2018, that figure has dropped to 38%.

Andy Howard said: “It is, of course, encouraging to see that investors’ long-held performance concerns about sustainable investing continue to subside. We have argued for many years that investing sustainably with a strong focus on robust returns should not be mutually exclusive. Indeed, thoughtful and considered approaches to sustainability are at the heart of the objective of delivering long-term investment returns.”

ESG becomes more social

While focus on environmental concerns continues, there’s evidence that institutional investors are now broadening their focus to include the “social” part of ESG.

The study found that 38% would now like to invest in funds with a specific goal such as sustainable infrastructure, while there is a four percentage point increase in those who would like to invest in funds that prioritise health and wellness as a sustainability goal.

Andy Howard, Global Head of Sustainable Investment, said:

“While the environmental aspect of ESG has long enjoyed a high profile, the Covid-19 crisis is turning the spotlight on the social element, such as companies’ treatment of their employees, suppliers and customers.

“At Schroders we believe that companies do not operate in a vacuum, they are part of the societies from which they draw their employees, to which they sell their products and under whose laws they compete.

“The crisis has exposed those companies that approach shareholder value as a trade-off against the interests of a wider group of stakeholders, and those which recognise that long-term, sustainable shareholder returns depend on strong stakeholder relationships.”

Building back better

As the world begins to emerge from an uncertain and unsettling period, the world’s institutional investors are positive, engaged and looking to the future.

It remains to be seen whether the current clouds on the horizon; inflation, global tension and supply issues with vaccines to the developing world, might blow this optimism off course.

Authors

Topics