The good, the bad, and the ugly of secondary public equity offerings

The stock market plays a crucial role in helping companies raise finance, but are these raises a good deal for investors?

Authors

Rolls Royce has recently raised around £2 billion in equity from investors, to repair its balance sheet from the effects of the pandemic. It is in good company.

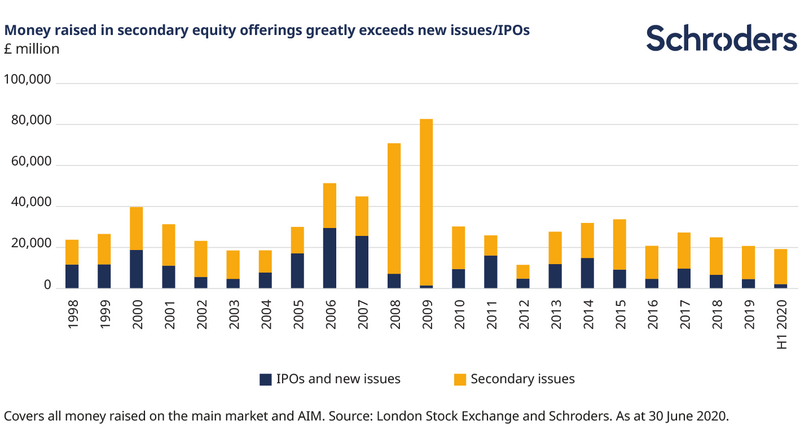

Existing listed companies raised around £17 billion on the London Stock Exchange in the first six months of 2020, double the average of the previous decade, and a record amount for the first half of the year, outside of the 2008-09 financial crisis.

Stock markets had been losing ground in the popularity stakes to private equity and debt, when it comes to a company’s choice of where to raise money. However, the trials brought on by Covid-19 have boosted their credentials.

This is good news for companies. However, for investors who back them, the results have been less clear cut.

Our research into over 1,600 secondary offerings that have taken place on the London Stock Exchange since 1998 found that a sizable proportion go on to perform very well but a similar proportion lose investors most of their money. If there was ever a time when good active management was needed, this is arguably it.

The good

The ability to raise finance relatively quickly from a large shareholder base has been an invaluable lifeline this year, with wider societal benefits.

It has helped keep companies afloat, people in jobs, and it has mitigated or avoided the need for companies to borrow their way through the pandemic. This provides a more resilient basis on which to deal with the challenges ahead. It can also act as an accelerator to the plans of those companies in growth-mode. The stock market is not ready to be written off just yet.

Nor is this just a flash in the pan. Since 1998, around twice as much has been raised via such secondary offerings – the issuance of new equity by existing public companies, most commonly via rights issues or placings – than initial public offerings/new issues. Since 2015 the equivalent multiple has been around three times.

2020 has seen secondaries power even further ahead. For the companies involved, a stock market listing retains tremendous value.

The good and the bad

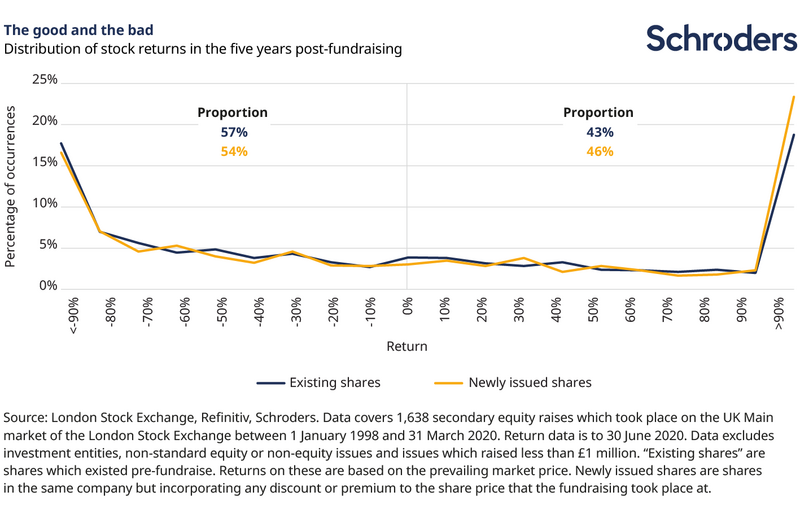

The disappointing news is that most companies that raise additional equity go on to underperform their sector (64% over three years and 66% over five years) – according to Schroders’ research into 1,638 secondary equity issues that took place on the UK main market of the London Stock Exchange between January 1998 and March 2020.

Shares bought as part of the capital raise have had better results, thanks to the ability to normally buy in at a discount. However, even allowing for this, most underperformed.

This does not mean that investors should avoid companies that are raising equity. It just means you need to be selective in which ones to back. Returns of these companies follow a bi-modal distribution: a relatively large proportion fall close to zero but an almost identical proportion deliver substantial returns.

In 18% of cases, a company’s share price fell by more than 90% in the five years after raising money, effectively wiping shareholders out. However, in 19% of cases, returns exceeded 90%. For shares bought as part of the equity issue, the proportion that delivered gains of more than 90% over the subsequent five years increases to 23%.

Performance is less favourable when assessed relative to a company’s sector. However, the same bi-modal distribution exists, with a high percentage delivering very good returns and a similar percentage delivering very bad returns.

The ugly

While clearly being relevant at the individual company level, many factors that you might expect to influence the likelihood of success or failure in general, turn out not to. Our analysis found no notable relationship with leverage or return on equity, nor whether either was rising or falling. Nor profit growth. Nor the size of a fundraising, or whether it takes place at a discount or premium to the share price, or the size of that discount or premium.

However, one factor that investors would be wise to pay attention to is refreshingly simple – whether a company is profitable or not. The distribution of outcomes has been more favourable (but still very wide) for profitable companies than loss-makers.

Loss makers have gone on to deliver lower medium-term upside, lower median/average performance, and worse downside risks than profitable companies. The difference is statistically significant.

For example, on a five year horizon, the average loss-making company that raised additional equity went on to underperform its sector by 38%.

In contrast, the average profitable fundraiser outperformed its by 4%. While top quartile profitable companies (the best performing 25%) outperformed their sector by an impressive 40%, their loss-making equivalents fell slightly short of theirs. Bottom quartile loss-makers (the worst performing 25%) also had poorer outcomes.

Loss-makers need not - nor should not - be avoided entirely, as some go on to deliver very good returns. The top 10% outperformed their sector by an impressive 81% over the five years post-raise. However, investors do need to be especially selective in which ones they back.

The need to be active

Existing public companies clearly value their ability to raise additional money on the stock market. Investors can also do well from backing these companies, but only if they take a very active approach in deciding which to support. Even within profitable companies, the range of outcomes is wide, with large proportions thriving but large also proportions struggling.

There is no substitute for rolling up your sleeves and carrying out proper fundamental analysis of the company in question, and its management. Not all fundraisings deserve to be backed. Creative destruction is healthy for economic growth. Due diligence and high levels of discrimination are essential. Passive investors do not have that luxury. They are forced to buy additional shares in response to every new equity issue, if they are to maintain an appropriate allocation to each stock.

The need to be active does not stop there. Once money has been raised, it is the responsibility of a company’s shareholders to hold management to account on how they execute on their strategy, how they spend that money, and, ultimately, on the sustainability of their business model. Not to do so would be complacent at best, negligent at worst.

Even passive investors cannot afford to be passive shareholders.

Information importante: Cette communication est destinée à des fins marketing. Ce document exprime les opinions de ses auteurs sur cette page. Ces opinions ne représentent pas nécessairement celles formulées ou reflétées dans d’autres supports de communication, présentations de stratégies ou de fonds de Schroders. Ce support n’est destiné qu’à des fins d’information et ne constitue nullement une publication à caractère promotionnel. Le support n’est pas destiné à représenter une offre ou une sollicitation d’achat ou de vente de tout instrument financier. Il n’est pas destiné à fournir, et ne doit pas être considéré comme un conseil comptable, juridique ou fiscal, ou des recommandations d’investissement. Il convient de ne pas se fier aux opinions et informations fournies dans le présent document pour réaliser des investissements individuels et/ou prendre des décisions stratégiques. Les performances passées ne constituent pas une indication fiable des résultats futurs. La valeur des investissements peut varier à la hausse comme à la baisse et n’est pas garantie. Tous les investissements comportent des risques, y compris celui de perte du principal. Schroders considère que les informations de la présente communication sont fiables, mais n’en garantit ni l’exhaustivité ni l’exactitude. Certaines informations citées ont été obtenues auprès de sources externes que nous estimons fiables. Nous déclinons toute responsabilité quant aux éventuelles erreurs commises par ou informations factuelles obtenues auprès de tierces parties, sachant que ces données peuvent changer en fonction des conditions de marché. Cela n’exclut en aucune manière la responsabilité de Schroders à l’égard de ses clients en vertu d’un quelconque système réglementaire. Les régions/secteurs sont présentés à titre d’illustration uniquement et ne doivent pas être considérés comme une recommandation d’achat ou de vente. Les opinions exprimées dans le présent support contiennent des énoncés prospectifs. Nous estimons que ces énoncés reposent sur nos anticipations et convictions dans des hypothèses raisonnables dans les limites de nos connaissances actuelles. Toutefois, aucune garantie ne peut être apportée quant à la réalisation future de ces anticipations et opinions. Les avis et opinions sont susceptibles de changer. Ce contenu est publié au Royaume-Uni par Schroder Investment Management Limited, 1 London Wall Place, London EC2Y 5AU. Société immatriculée en Angleterre sous le numéro 1893220. Agréé et réglementé par la Financial Conduct Authority.

Authors

Thèmes