A Tale of Two Offices: how WFH has changed investing in office real estate

Offices are not going extinct, but investing in them has changed permanently and a two-tier market has developed.

Patchy broadband, children interrupting Zoom calls, speaking while on mute – the trials of working from home (WFH) have been much discussed over the last couple of years.

But few groups of people have more hotly debated the “new normal” for working than real estate investors.

Particularly, how will WFH impact the take up and value of offices?

Last year we wrote about how all real estate assets have become “operational”. We meant by this that the income and long-term performance from them is highly correlated with the success of the operations of the buildings’ tenants. Not just the length of the lease contract.

At the same time, real estate assets do not just provide a roof over the tenant’s head or a place to put a desk. The way they are operated is highly relevant to the tenant’s business model and success.

This has become true for all real estate types, but definitely for offices. Before the pandemic, flexible office providers that catered to the specific needs of tenants were gaining traction.

But now, if people are no longer going into the office as often, should we expect the office market generally to go into long-term decline?

We think it is too simplistic to assume that less time in the office means less office demand. More importantly, it is too simplistic to talk about only one office market.

Overall office demand: short-term

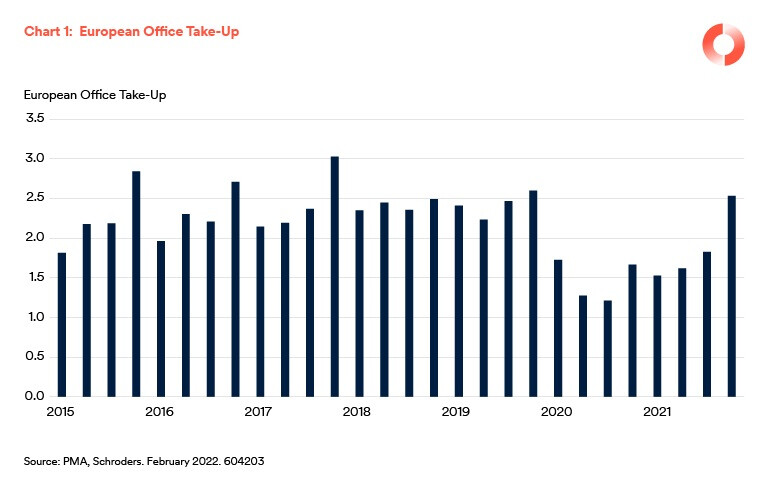

Last year saw a strong recovery in office demand across Europe as economies emerged from the first wave of lockdowns. Take-up in the second half of 2021 was 50% higher than in the same period of 2020, but still 20% below its pre-pandemic average. In addition, the increase in office vacancy slowed sharply, as the amount of surplus space which companies wish to sub-let stabilised.

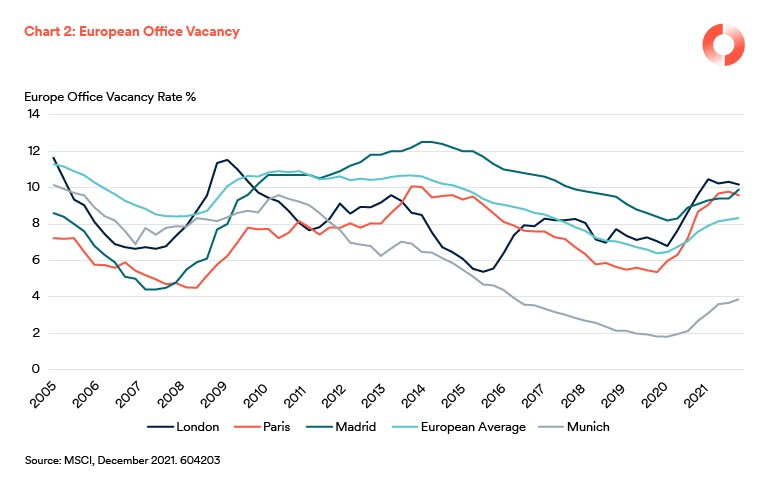

The average office vacancy rate in Europe, at 8.3% in September 2021, was only marginally higher than in June (8.1%) and well below the peak of 10.9% reached in 2010, following the global financial crisis (GFC).

In the short-term, we have estimated that hybrid working - people working part of the week at home and part in the office - will reduce European office demand by an average of around 15% compared with 2019.

Demand is “sticky” as a result of existing lease contracts. At the same time, new business models are being tested. There is also a need to allow for “peak days” when most people are in the office (assuming staff can choose) together. All this means that demand will decline by less than the amount of time actually spent in the office.

Across Europe, we anticipate that the following cities are likely to be most affected in 2022-2023.

- Financial centres (e.g. London, Zurich). In part this reflects a catch-up process because financial companies were slower than tech firms to adopt remote working before the pandemic. In part it also reflects our view that other occupiers such as government agencies, law firms, life sciences are less willing, or able to let staff work from home.

- Cities with relatively long average commute times, typically bigger, more congested cities (e.g. Paris, Rome)

- Cities with an older office stock which provide a less attractive working environment (e.g. Brussels, Copenhagen).

Overall office demand: long-term

General office demand is therefore likely to be lower in the next couple of years than in 2019. In the long-term though, it is likely to recover thanks to the growth in employment in sectors such as tech, media and professional services.

Oxford Economic forecasts that office employment in Europe’s major cities will on increase on average by 1% per annum between 2022-2027, although there will be a lot of variation across different cities (see chart above). To some extent, the variation in forecast employment growth reflects cities’ economic structure.

The Nordic cities have a relatively high exposure to tech. Manchester has strength in professional services. Brussels and Rome are dominated by government occupiers. Madrid and Barcelona have a low exposure to financial services.

However, economic structure is not the whole story. The reason Lyon stands out is that its professional services are growing faster than in other cities, probably due to a transfer of work from Paris. Similarly, Luxembourg is a financial centre, but its bias towards asset management rather than banking means employment in financial services is forecast to grow rather than shrink. Finally, demographics also play a part. The modest increase in office jobs in most German cities over the next five years (except Berlin) is largely due to an ageing population, such that the number of people of working age is forecast to be flat, or fall slightly.

In addition, we expect that the trend over the last 20 years, of cramming more people into the same space, will reverse post-Covid. We expect the next 5-10 years will see a small increase in space per worker in cities in France, Spain and the UK, where space is tightest.

Combining all these factors we estimate that by 2027, office demand in Europe will be 10% lower than in 2019, but on an upward trend.

The cities which are likely to be most badly hit by the shift to hybrid working are Brussels, Dusseldorf and Rome. Here the combination of slow employment growth, longer commutes (especially in Brussels and Rome) and generally older office stock with poorer facilities will likely weigh.

By contrast, Luxembourg, Lyon, Madrid and Manchester are likely to see the strongest recovery in demand over the next five years thanks to strong employment growth and a relatively modern office stock.

Not just location, location, location

Drilling into more detail, we can clearly see that we can not speak of one office market anymore.

If we look at the type of space that occupiers require, we can see that the focus on “prime” offices, which was already growing before the pandemic, has become even more pronounced. We define “prime” as a new, or recently refurbished office, which is well specified, energy efficient, located in the central business district (CBD). These offices also provide significant additional services to its tenants to support their business model, therefore increasing the likely longevity and sustainability of income from the asset.

In Amsterdam, office vacancy is now clearly highest in fringe locations (e.g. ArenA, Sloterdijk) where demand was increasing significantly before lockdown (based on comparatively lower rental pricing). This is as a result of the lack of services and facilities for tenants being offered.

Conversely, vacancy in Zuidas, the main office district, initially rose in 2020, but then fell rapidly through 2021 to 2%. The Zuidas area has significantly invested into new or re-created sustainable office stock, as well as upgrading the area to provide significant additional services to tenants.

A similar pattern is evident in office submarkets of London, Munich and Paris. Location-wise, unlike in the US, there are few signs in Europe that the pandemic has prompted companies to relocate from big city centres to suburban office parks, or smaller cities.

Occupiers are becoming more and more demanding about specifications. In part this can be attributed to Covid-19 and the eagerness of employers to tempt staff back into the office in order to foster ideas and a shared culture.

While the use of high quality offices as a lever to attract skilled staff is not new, the emphasis on state of the art air conditioning, excellent Wifi and video conferencing, sufficient break-out rooms, bicycle stores and other amenities has grown significantly over the last two years.

The need for desks is falling as people do more individual work at home. But the space required for meeting rooms and collaboration is rising and now accounts for 25-40% of space, against 10-15% a few years ago.

The other key driver behind the demand for higher quality space is sustainability. The EU and UK have pledged to cut carbon emissions in 2030 by 55% and 68% respectively, compared with 1990 levels. One of the main ways this will need to be achieved is by improving the energy efficiency of buildings. Previous doubts that occupiers were not prepared to contribute and pay a higher rent for special features have evaporated. Such features might include solar panels, green walls, sensors which give people control over heating, lighting and ventilation, smart glass and better insulation have evaporated.

Last year’s spike in oil and gas prices has given occupiers a further reason to reduce energy consumption. In Germany “green” offices accounted for 31% of take-up in city centres over the 12 months to June 2021, despite accounting for only 9% of total floorspace. In the City of London, the percentage was over 70%.

The “haves and have nots”; how cities are split on office demand

The two-tier nature of demand has led to a strong and, in our view, persistent divergence in prime and secondary office rents and values.

Several cities saw an increase in prime rents in 2021, including Amsterdam, Frankfurt, London and Paris, whereas secondary rents either fell, or were at best flat. The recent low level of development in many European cities has provided further support for prime rents.

Not surprisingly, this divergence by quality was echoed in the investment market. Strong competition among investors for offices with secure income meant that prime yields fell by 0.1-0.25% in most cities in 2021. Meanwhile, average grade offices yields rose, depressing capital values.

Of course, a flight to quality during a period of uncertainty is nothing new. We saw a similar polarisation in European office markets after the internet bubble burst in 2000 and again, during the GFC.

Let's assume that a low equivalent yield (i.e. cap rate) is a proxy for prime offices and a high equivalent yield is a proxy for secondary offices. If so, MSCI UK data suggest that prime offices in London outperformed secondary offices by a wide margin between 2008-2009, but then fell behind through 2010-2015, as secondary office rents started to recover, albeit from a lower level and as investors moved up the risk curve. This pattern was repeated in office markets outside London, although with a delay because of a slower recovery in demand and secondary rents.

Will Europe’s two-tier office market persist?

Given past history it might seem reasonable to assume that prime offices will cease to outperform once the pandemic ends. However, we think this view overlooks the fact that the dynamics which determine the relative performance of prime and secondary have changed.

In the past, the main drivers were cyclical and once demand had started to recover and prime rents had risen, occupiers were more willing to compromise and take secondary space at a lower price. Similarly, once vacancy had started to fall, investors were more willing to buy offices with short unexpired lease terms, or refurbishment opportunities.

While those cyclical drivers have not disappeared, we suspect they will be trumped by a number of long-term structural forces working against secondary offices.

First, the pressure from occupiers and from governments to cut carbon emissions and make buildings more resilient to climate change (e.g. water recycling, flood prevention) will only intensify. Carbon taxes on heating fuel will steadily increase and although the Netherlands and UK are the only countries which have so far banned the letting of buildings with poor energy ratings, other European governments are likely to follow suit. Furthermore, the recent jump in construction costs means that some offices in peripheral locations risk becoming stranded assets, because it is no longer viable to upgrade them.

Second, the move to hybrid working is probably more of a problem for the secondary office market.

Secondary offices tend to attract more cost-conscious occupiers who are more likely to try to economise on office space by asking staff to work remotely. These occupiers might decide to have no office, or upgrade to smaller, higher quality office for the same cost, but use this space more flexibly and take out different building services (flexible office space, shared concierge, etc) to suit their business model.

Third, new software such as robotic process automation, blockchain and voice recognition will cut demand for call centres and back offices.

The death of the office has been greatly exaggerated

We can not speak about one office market any longer. The office market as we knew it is in transition, not structural decline across the board.

While some commentators have drawn parallels with the retail market, we think it is a false analogy because office employment will continue to grow and because remote working does nothing to boost top line revenue growth.

Whereas the internet enables retailers to both cut costs and reach new customers, remote working only improves the bottom line for office occupiers. Indeed, there is a risk that it could jeopardise long-term revenue growth if prolonged working from home reduces innovation and productivity.

We also believe that office demand will continue to polarise and that current yields on secondary offices do not yet adequately reflect the increased risks of obsolescence from sustainability, hybrid working and new technology. Accordingly, we expect that prime offices will outperform secondary offices in most European cities through the first half of the decade.

Subscreva o nosso conteúdo

Visite o nosso centro de preferências e escolha que informação deseja receber por parte da Schroders.

Topics