Is the time up for US equities’ leadership?

It's unlikely that the US stock market will continue to outperform over the coming decade. Here's why.

Authors

US stock market exceptionalism has been a defining feature of the previous decade. Since the Global Financial Crisis, US equities achieved an annualised return of 13%, far outstripping global equities’ 6% annualised return (as measured by the MSCI USA Index and MSCI AC World ex US Index respectively, in US dollar terms).

Even in the wake of the Covid-19 outbreak, this trend has remained intact, leading some investors to question whether they should even bother owning any non-US equities at all.

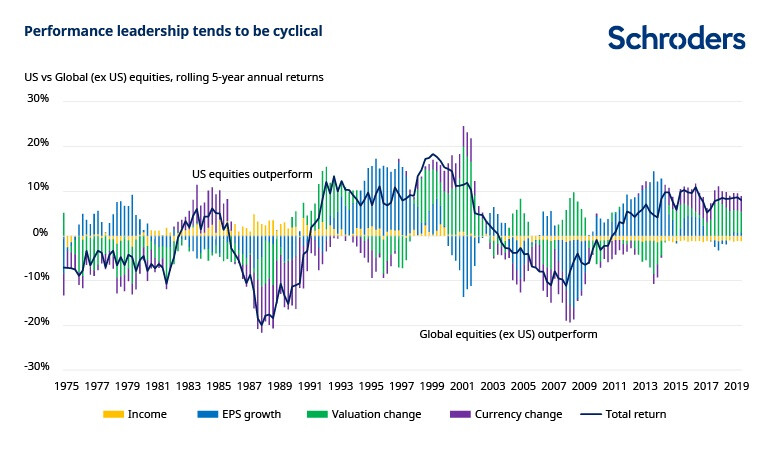

However, those who expect this trend to continue over the coming decade are setting themselves up for potential disappointment. After all, the winners and losers, both within and across markets, fluctuate over time. This time shouldn’t be any different.

Besides, a shift towards non-US equities is long overdue. And while timing this inflection point is difficult, all the signs tell us that gravity will eventually bring US equities back down to earth.

- The full research paper is available as a PDF at the foot of this article.

US earnings advantage has disappeared

The main reason US equities have done so well is because of their superior profit growth. For example, from 2009 to 2014, US earnings-per-share (EPS) grew at 17% per year compared with only 7% outside the US. This is shown in the chart below.

Past performance is not a guide to future performance and may not be repeated.

Source: Refinitiv Datastream and Schroders. Data to 30th April 2020. Notes : US equities = MSCI USA Index, Global equities = MSCI World ex US Index $.

The problem is that this earnings growth advantage has pretty much disappeared. Since 2015, nearly all of the relative outperformance has been driven by a combination of valuation multiple expansion and dollar strength. Valuations and the dollar can always climb higher, but not indefinitely.

Markets have justified this valuation premium because US firms have been able to reinvest their profits at increasingly higher reinvestment rates. However, the secular forces supporting this trend such as globalisation, lax anti-trust enforcement and international tax arbitrage have either stalled or are reversing.

US share prices are no longer in sync with earnings

For most of the post-crisis period, US outperformance has moved in tandem with relative earnings expectations. However, recently the gap between relative returns and earnings expectations has widened significantly.

Past performance is not a guide to future performance and may not be repeated. Source: Refinitiv Datastream and Schroders. Data to 1 May 2020. Notes: US equities = MSCI USA Index, Global equities = MSCI AC World ex US Index $.

This is not sustainable. At some point, earnings expectations will need to catch up or US stock prices must correct.

The price you pay matters for future returns

One consequence of this is that valuations are stretched to levels which would have historically foreshadowed low returns for US equities versus the rest of the world. For example, US share prices trade at 25x their cyclically-adjusted historical earnings (CAPE) compared to only 13x for global equities. The long-term outlook for the US relative to other markets no longer seems attractive.

The winner’s curse

The US is home to some of the most successful companies in the world, including firms such as Amazon, Microsoft, Apple, Google and Facebook. Together, they have delivered significant profit growth and technological innovation.

However, these companies have become so large that they are essentially driving the market. Their combined market-cap weight has more than doubled from roughly 8% of the S&P 500 Index in 2015 to nearly 20% today.

A market this narrow should give cause for concern. The bigger they get, the harder it becomes for them to replicate that performance. This is because once a company dominates an industry, it can only grow as fast as the market size grows.

The only way they can continue to justify their growth multiples is by developing other game-changing products, or leveraging their existing resources to branch out into other services. But there is no guarantee they will succeed.

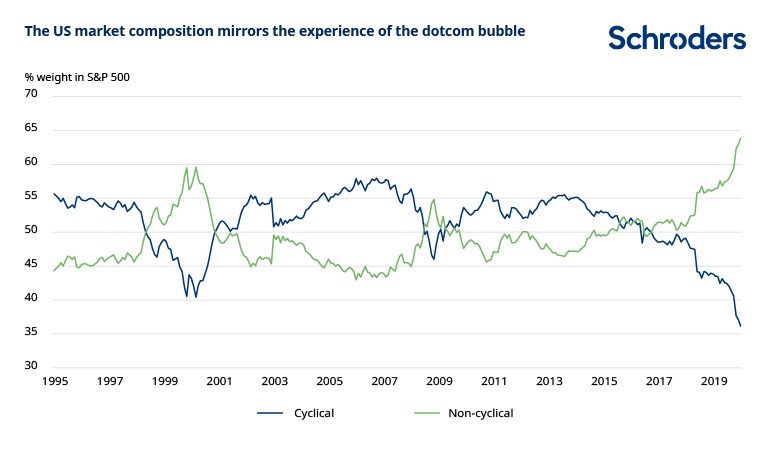

Cheap exposure to a cyclical recovery sits outside the US

Global equities are especially attractive now given their higher economic sensitivity. For example, as at 31 May 2020, cyclical stocks represented 58% of the MSCI All-Country World ex US Index, but only 36% of the S&P 500 Index.

Typically, cyclicals perform best after the economic cycle bottoms, so a lower relative weighting in this segment could limit the rebound in US equities once global growth recovers.

Source: Refinitiv Datastream and Schroders. Data to 31st May 2020. Notes: cyclical = materials, industrials, consumer discretionary, energy, financials, real estate. Non-cyclical = utilities, IT, consumer staples, health care, communication services.

Avoid putting all your eggs in one basket

The last decade has belonged to the US but history shows that performance leadership is cyclical. Investors should heed this warning carefully.

Although we can never really claim to know in foresight, the way we do in hindsight, why and how these cycles of outperformance shift, we do know that conditions are ripe for a reversal.

Earnings growth differentials have flattened, valuations look stretched, market concentration has increased and US cyclical exposure to a global recovery is limited.

Against this backdrop, investors may be wise to diversify their equity portfolio outside the US over the coming decade.

Please find a PDF of our research paper below.

Subscreva o nosso conteúdo

Visite o nosso centro de preferências e escolha que informação deseja receber por parte da Schroders.

Authors

Topics