Securitised credit: Where we’re going, there are no roads (part 2)

Focusing on fundamentals, structure and valuation should help investors to navigate a future for which there is no precedent.

In part 1 of this article, we referenced a quote from the 1980s movie trilogy “Back to the Future”, and we took a little liberty in using “where we’re going there are no roads”…

In fact, the correct quote from the Back to the Future trilogy is, “Roads, where we’re going we don’t need roads”.

We concluded that paper with a quote of our own, which sets the framework in this paper for how one navigates forward in a market with no prior precedent:

“So, while we are going where it feels there are no roads, we can still cut the trail. Understanding that uncertainty need not create paralysis, nor should it result in rash bet making, or blind faith in old ‘rules of thumb’. Maintaining an awareness for when uncertainty rises and falls is critical, and understanding that, even through these phases, opportunities with conviction can be identified through an examination of fundamentals, structure and valuation.”

Navigating without roads

The economy is facing an exogenous shock that has caused a cessation of economic activity unseen in prior economic recessions. To control the spread of Covid-19, the economy has been shut down. The shutdown itself is a material economic problem with dire consequences for businesses and for consumers. In a matter of weeks, a decades-worth of payroll growth has been erased.

There has been a material and rapid response from central banks to ease interest rates and to alleviate a liquidity crisis. There have been fiscal stimulus packages aimed at bridging a temporary period while economic activity remains low. However, without a cure, and without antibody testing, and with the lockdown lasting for months, not for weeks, it is likely there will be both economic and employment destruction that persists well beyond a temporary period.

Behavioural change may be lasting, and is very likely to significantly impact consumers, their propensity to spend, and their propensity to save. In light of these potential lasting impacts, even considering the massive amount of monetary and fiscal stimulus, we believe there will be material increases in real credit issues, or defaults, as there is leverage in the system that will be exposed. At the very least, we are moving through a period of uncertainty, where history may not serve to be a relevant proxy.

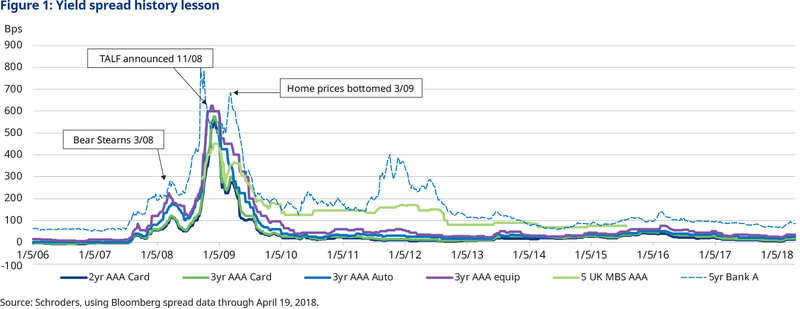

In March 2008, we saw the failures of Bear Stearns. And then in September, the failures of Lehman Brothers, Fannie Mae, Freddie Mac, even a bailout of AIG. After these stunning events, spreads had widened, in particular for mortgage credit, yield spreads appeared wide, mortgage credit looked “cheap” on a historical basis.

Does any of this sound familiar?

Back in 2008, investors looked to history for precedent and felt that history gave us reliable information as to the forward path. Historically true facts, such as “home prices have never declined at a national level”, and “home owners always pay their mortgage with first priority”, were thrown around as justification that wide spreads represented an opportunity. Investors then spent the next 9-12 months learning that home prices could decline nationally, to the tune of 40%, and homeowners would pay their auto debt, and default on their homes, which led to many loans that were “underwater”, or loans on a home with a lower market value than the amount of the loan. It was a painful lesson that mortgage credit investments were not cheap in 2008. In fact, home prices could go down 40% at a national level, and, in fact, homeowners would default on home loans if they felt their homes have fallen in value. Consumer behaviour had changed. It was a lesson well learned, and very relevant now, in 2020.

In uncertain times, it’s best not to be too dependent on a given recovery path; in fact, we would argue the potential range of outcomes remains very wide. But as we’ve seen in almost every period of crisis, leverage is a problem. Leverage enhances sensitivity and reduces the cushion to variation. There are many types of leverage at work: operating leverage, asset leverage, borrower leverage, structural leverage or financial leverage. Throughout this economic cycle, there will be winners and losers, and we continue to believe it will come down to leverage.

We also believe that support for the markets in the form of liquidity support, like temporary loans, buys a little time to help otherwise “good” borrowers or businesses from becoming collateral damage. It does not solve leverage problems. That requires a different medicine.

Fundamentals

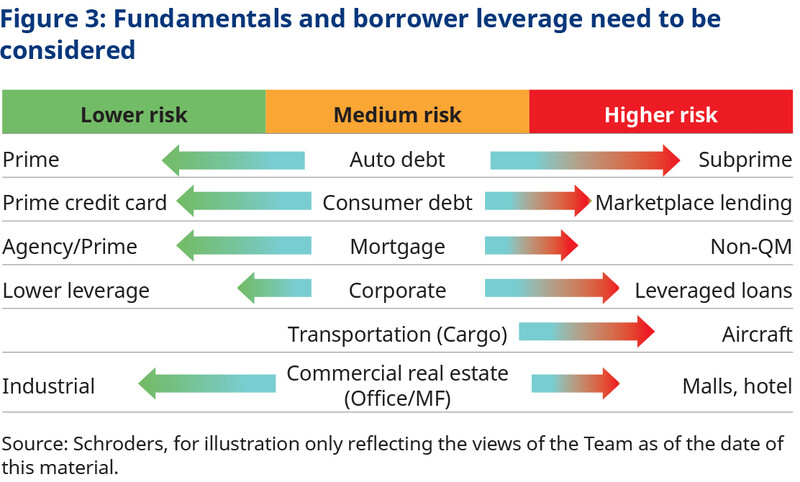

So, as we embark upon a path forward, we begin by looking for leverage, beginning with an examination of sector fundamentals. How leveraged is the corporation, the borrower, or the asset? Following the last financial crisis, the regulation of the banks and consumer protectionism resulted in a de-leveraging of the US consumer.

By contrast, US corporate debt issuance grew substantially, and the investment-grade universe saw a material decline in quality with a material increase in the percentage of BBB-rated corporations, relative to those corporations rated higher than BBB. In our view, the corporation was more leveraged than the consumer.

That said, a black-versus-white approach is too generic. Some industries and companies currently have lower leverage, whereas some have extraordinarily high leverage. Likewise, not all consumers are equally well off.

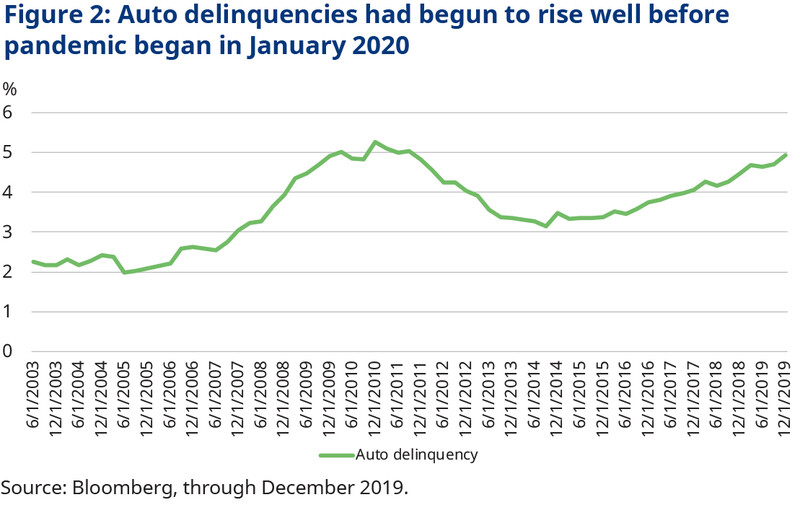

Using auto debt as an example, there are important intra-sector differences. In fact, auto loan delinquency levels were rising even before the economic decline associated with Covid-19. The increase in delinquency rates for auto loans, over the last two years, is attributable to a change in the overall lending market, and an increase in subprime auto lending. Loans to weaker, more sensitive borrowers, had been driving the delinquency increase. These consumers are the more “leveraged” consumers, categorized by few reserves and an increased sensitivity to economic circumstance.

If one was worried about the economy being “later cycle”, the best choice would not only be the consumer over corporation, generically, but specifically, the choice would be a prime consumer, over a subprime consumer, ceteris paribus.

Further, we would argue that larger, more established, debt classes like mortgages, auto loans and credit card receivables not only offer better transparency than their esoteric cousins, but they offer more established regulatory practices and more significant sponsors and counterparties, such as public companies. As well, being materially important consumer debt markets, crucial to consumer credit, they are among the more likely markets to get some type of federal support, directly, or indirectly, through consumer support.

Newer forms of debt such as marketplace lending and internet lending, as well as non-QM (qualified mortgage) lending, are less regulated and have smaller, private sponsors, are smaller markets and may not be considered, by the government, as worth supporting.

As well, screening for leverage, lending practices and market size, should not be a new process. It should be imbedded in the way an investor evaluates fundamentals, structure and valuation.

Structure

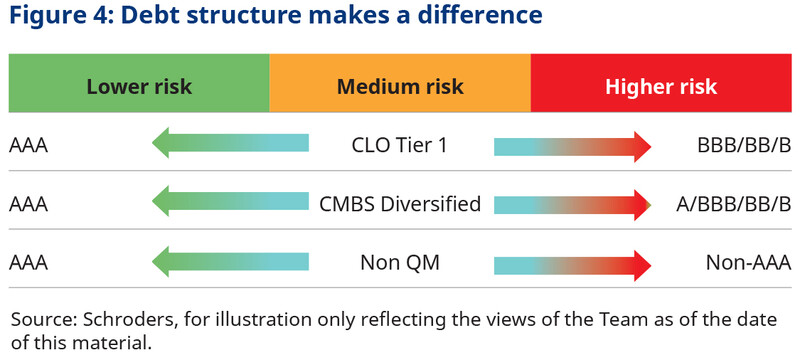

The next step is to look at any introduction of addition leverage, or sensitivity, or protection, created through a tiered capital structure. Here, structured products, or securitized credit, can be very unique. Through a tiered capital structure, cashflow can first be directed to a senior security and then subsequently to one or more junior securities. The securities that are paid first in priority are senior classes. The senior class can be considered protected, in that the securities have additional cushion to absorb unexpected declines in cashflows from the assets. The cushion comes in the form of considerable credit support.

The “credit support” or cushion is coming from the more junior classes. They are the first to absorb losses, and they can often have their available cashflow diverted to the senior classes during times of lower than anticipated cashflow from the underlying loans, or receivables. These junior classes, then, are securities with more sensitivity to the underlying asset and its performance.

In today’s environment of uncertainty, often the structure can be used wisely. Notes more senior in the capital structure offer reduced sensitivity to changes in the performance of the underlying borrowers; this reduced sensitivity is very important in the early phases of an economic decline, particularly one with high uncertainty.

As an example, a leveraged loan may be considered a more leveraged asset, with greater risk of default in an economic decline. The most senior class in a Collateralized Loan Obligation (CLO) however, has more than 35% credit support to protect against increasing defaults, or to protect against declining recoveries realized from the defaulted loans. The more junior classes, often rated BBB, BB, etc., have much less support, often as little as 8%.

As such, these classes are exposed to the weaker end of the collateral pool. Should a pool have exposure of 15% to high risk sectors (energy, leisure, travel, gaming and airlines often tally 15%), it is easy to see that in an environment of deteriorating quality and lower recoveries, these classes will be sensitive to these riskier exposures. This is the double-edge sword of structure. It can be used to create protection, or to create enhanced sensitivity. At different times, each of these characteristics can be desirable.But in an uncertain environment, clearly being more sensitive equates to being more path dependent.

Valuation

The third leg of the stool is valuation. Often the great equalizer, valuation (or price discount), can also help to build in cushion to downside risk. For example, if you pay 50 cents on the dollar for a bond, you do not have to get par back to earn an attractive return.

But, by the same token, a price of 50 cents of the dollar is not always “cheap”. We discourage the use of historical pricing levels as a proxy for “cheap” or “rich”. Today’s cashflows could follow a different path than those of the prior crisis. And if the price of security goes to zero, rather than par, a price of $50-60 is not a very “cheap” deal.

Valuation discounts can correct the negatively asymmetric proposition that most par-priced bonds represent. That is return potential say, with a par-priced bond, over the bond’s life, the best return you can earn is your “coupon”. A win is getting your coupon, and getting your par back, there is no upside. In the worst case, you can have a full loss of par value. This is the asymmetry of a par-priced bond, and for some, more sensitive cashflows, we say “par is never the right price”. If you own a return with material risk of par loss, similar to the risk you take in equity, you should be looking for a return with upside to offset the potential downside. With a valuation discount, you can get a more symmetrical return profile.

For example, consider a bond that expected defaults might impact, the market may think there is a chance of a 40% loss of par. If you buy this bond at $50-60, you have the potential for price upside if losses are less than 40%, and a large upside return if you recover $100.

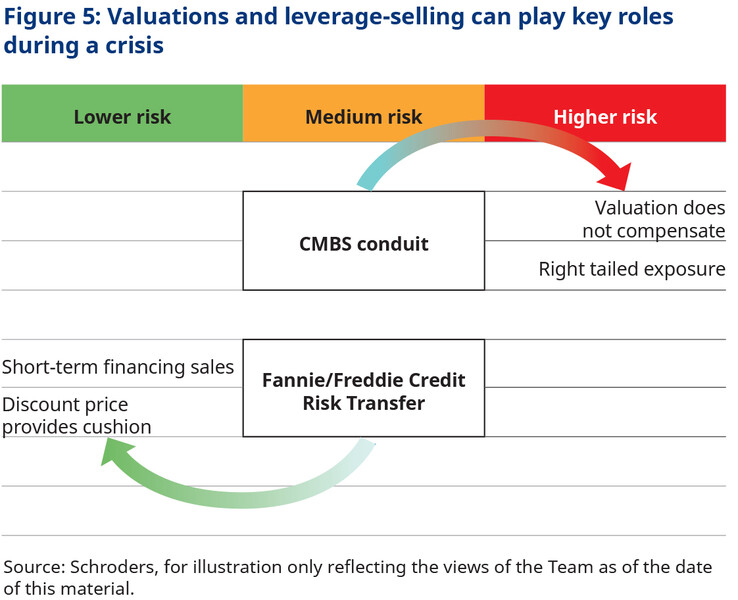

Whereas fundamentals and structural change typically happen more slowly, valuations can change quickly, and they can change for a number of reasons. Prices decline when yield premiums increase as the market begins to price in more elevated default rates, or due to excess supply, or diminished demand. Selling due to liquidity reasons can change the supply of bonds and the demand for bonds quickly.

As well, to the extent bonds are held by owners that utilize financial leverage, and financing arrangements require mark-to-market adjustments and margin calls, there is potential for forced selling. We have seen each of these pressures exert powerful pressure on valuations over the last six weeks, creating valuation opportunities within groups of securities with strong fundamentals and supportive structure.

Valuations can also change to the extent that regulation drives a required deleveraging, or a changing of hands, as was the case for banks, in 2008-2012. In the early days of “new” challenges, defaults/losses can be underestimated; very likely this was why it took until March 2009 (the bottom of home prices) to see the low point in US non-agency RMBS prices.

We expect to see continued change in valuation pressures over the coming months as fundamentals evolve, as impairments impact selling and as we see additional pressured selling driven by margin calls for REITs, hedge funds, and warehouse lines, or due to fund redemptions. A change in price can be material enough to offset even dire expectations for downside cash flows. This was the lesson learned buying subprime MBS in 2009-2010, these out-of-favour assets turned out to be one of the most attractive investment opportunities due to discount pricing, despite high default rates and severe downgrades.

Final thoughts

The intersection of fundamentals, structure and valuation help us navigate different degrees of uncertainty

With strong positives in fundamentals, structure AND valuation, cashflows can tolerate a greater amount of variation and become built to last. Built-to-last cashflows are, as we paraphrased in our Part 1 paper, like the proverbial boxer in the ring that can take a number of chin shots and remain standing. This is what is necessary and desirable when uncertainty is high. With adequate flexibility in an investment strategy, an investor can use the combination of fundamentals, structure and valuation to maintain their ability, even in uncertain times, to create conviction in an opportunity.

Then, as the economic corrections play out, the range of outcomes become better understood, expectations or parameters can be narrowed, conviction can be built across a new or a wider range of opportunities. In our view, the higher risk becomes lower risk as defaults are more readily assessed, recoveries are better understood, and pricing has reached more appropriate levels.

As well, as the “financial” side of the crisis unfolds, and as inefficiencies impact the flow of capital, opportunities to lend, or the ability to provide capital directly, present as well.

Subscreva o nosso conteúdo

Visite o nosso centro de preferências e escolha que informação deseja receber por parte da Schroders.

Topics