Seven-year asset class forecast returns: 2017

Returns face further compression and investors seeking positive real returns would be advised to look at riskier assets: credit, equities and alternatives.

Authors

Our seven-year returns forecast largely builds on the same methodology that has been applied in previous years, as explained in the appendix to this document; and has been updated in line with current market conditions and changes to the forecasts provided by the Global Economics team.

This document compares our current return forecasts to those last published in July 2016.

One key change this year has been a change to our methodology for forecasting credit returns, to incorporate the effects of quantitative easing (QE). A full description can be found in the appendix.

Summary

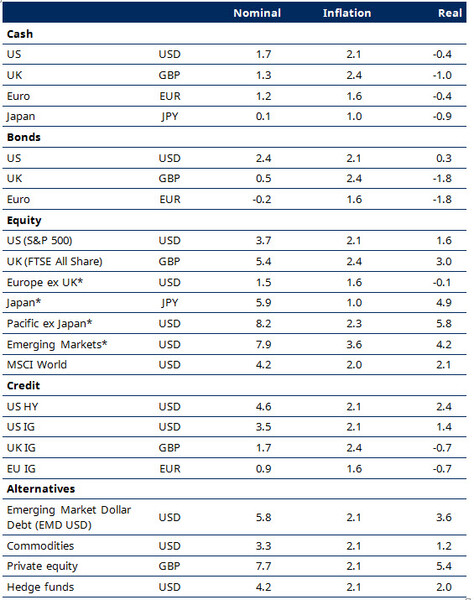

Table 1 below shows our forecast returns for the 2017–24 period. Cash and bond returns are largely expected to be negative in real terms, unsurprising perhaps given the continued low rate environment.

Investors seeking positive real returns would be advised to look at riskier assets: credit, equities and alternatives.

However, even here it seems positive returns are not assured. European credit and equities, for example, are both expected to yield negative real returns over the forecast horizon.

Table 1: Seven-year asset class forecasts (2017-2024), % per annum

Note: *Thomson Datastream’s indices. Source: Schroders Economics Group, Schroders Property Group, July 2017.

Please find the full analysis of asset class returns at the link below.

Subscreva o nosso conteúdo

Visite o nosso centro de preferências e escolha que informação deseja receber por parte da Schroders.

Authors

Topics