Why tariff reversal won’t save the US

Since the imposition of Trump era tariffs had no obvious impact on overall US inflation, or Chinese exports, it is not clear what rolling them back might achieve.

Authors

Pressure is ratcheting up on President Joe Biden to reverse the collapse in his popularity ahead of mid-term elections on 8th November by tackling rampant inflation. This week he called on Congress to suspend federal taxes on fuel and there have been hints that tariffs on goods imported from China imposed by the Trump administration will soon be rolled back.

It will be politically challenging for Biden to reverse all of the tariffs on Chinese goods. As we noted at the time of his election victory, hawkish policies towards China have become popular on both sides of the aisle in Congress. As a result, appearing to “go soft” on Beijing and opening the door for even more Chinese exports could be a major own goal – especially if lowering tariffs fails to bring down red hot inflation.

Looking at the headline data, it is easy to arrive at the conclusion that rolling back tariffs would help to lower inflation in the US and improve the fortunes of exporters in China. After all, as the charts below show, a weighted average of the 11 categories of the US CPI basket that faced tariffs rose by 2.5% during the initial phase of the trade war. They’ve increased by even more in recent years.

Meanwhile, China’s bilateral trade surplus with the US fell by about $60 billion in the nine months to March 2020 on a 12-month rolling basis. On the face of it, then, it makes intuitive sense that lowering tariffs would reverse these trends.

However, once we start digging into the data it becomes less obvious that rolling back tariffs would have much of a positive impact on either US prices or Chinese exports.

Starting with US inflation, while the price of goods that faced tariffs did clearly rise during the trade war, the 11 broad categories accounted for less than 5% of the US core CPI basket. As a result, the 2.5% increase in prices contributed only about 0.1 percentage point to overall core inflation during the period. Given that the prices of other goods barely budged, overall core inflation remained low and stable at around 2% as tariffs were imposed.

Admittedly, the prices of those goods that face tariffs have risen sharply more recently, up by about 15% since the start of 2020. It could be argued that there was simply a lag between tariffs being put in place and the price pressures reaching consumers. However, while difficult to disentangle, it seems that these increases are as much to do with general global price pressures than the tariffs themselves. After all, core goods inflation has soared during the pandemic as the supply of many products was unable to keep pace with rampant demand.

Either way, it is not obvious that tariffs led to particularly strong upward pressure on goods prices in the US and there are probably a couple of key reasons for this.

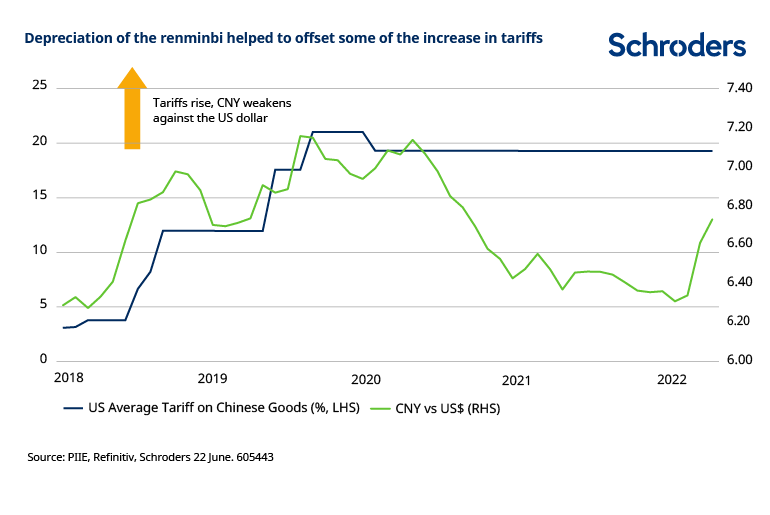

For a start, at least some of the increase in tariffs was absorbed. It is hard to prove conclusively that levies were absorbed into corporate margins, but it is certainly the case that a depreciation of the Chinese renminbi helped to offset the impact of tariffs. As the chart below shows, the renminbi depreciated by more than 10% to around 7.20/$ as tariffs were imposed. That helped to ensure that growth in US import prices from China actually eased during the trade war.

Meanwhile, it also appears that Chinese exporters were able to circumvent tariffs by shipping goods via third party countries. For example, China’s official trade statistics show that the trade surplus with the US fell by almost $60 billion during the trade war.

Almost half of the decline, however, was offset by an increased trade surplus with other parts of Asia – particularly South Korea, Vietnam and the Philippines. The combination of these factors helped to ensure that China’s overall trade balance continued to climb during the trade war even as tariffs increased.

The upshot of all of this is that while the removal of tariffs may offer some marginal relief to price pressures on certain goods, it is unlikely to bring headline inflation crashing down. Goods inflation does appear to have started to roll over in recent months. However, there are at least three reasons to think that inflation will be a problem for a while longer if bottlenecks persist, commodity prices remain elevated and service sector inflation picks up.

By the same token, there is little to suggest that rolling back tariffs will significantly improve the fortunes of China’s export sector. The sector faces a steep decline in activity in the months ahead as new orders have fallen away.

Subscreva o nosso conteúdo

Visite o nosso centro de preferências e escolha que informação deseja receber por parte da Schroders.

Authors

Topics