CIO Lens Q2 2026: Building diversified portfolios for uncertain times

In this quarter's CIO Lens, our investment experts highlight the need for resilient portfolios as developments in the Middle East increase uncertainty for investors.

Autheurs

In this quarter's CIO Lens:

Click the play button above to watch Johanna's latest video or read her column below:

Recent weeks have been riddled with uncertainty caused by the conflict in Iran and the significant impact on energy supplies. At the same time, we are dealing with unprecedented AI disruption, with uncertain consequences for labour markets and business models.

So how do we devise a strategy? When we are dealing with events and trends which might be difficult to price, we try to step back and think about what aspects of the market we can be more certain about. This allows us to build more resilient portfolios.

What do I know for sure?

In recent years we have moved from a globalised world prone to deflationary shocks to a de-globalised, more geopolitically uncertain world prone to inflationary shocks. Against this backdrop, commodities and real assets provide diversification benefits while bonds are less effective shock absorbers. We were already concerned that inflationary risk was underpriced because of the level of fiscal stimulus in the West. The conflict in Iran amplifies the inflation risk but the consequence for our view on government bonds is the same - we maintain a negative bias.

Credit spreads in the US are priced for perfection, not volatility. Yield-hungry investors continue to absorb elevated issuance, sustaining a finely balanced equilibrium, as hyperscalers fund the AI build-out. The expansion of private credit, as it has stepped into the shoes of the banks, adds opacity.

The labour market continues to be the key driver of central bank policy, particularly in the US. Although energy price spikes may cause inflationary pressure, the Federal Reserve is likely to lean dovish if the labour market weakens, particularly given uncertainty over the disruptive impact of AI. So keep watching wage growth and jobless claims and don't assume that this energy price shock will be followed by a rate shock.

Preparing for the unexpected

Instead of asking "what will happen next?", investors should ask "how would my portfolio behave if something unexpected happens?". At any moment market pricing represents a probability weighted range of scenarios. Thinking about the shape of that distribution can help to assess the likely correlation between asset classes and build more diversified and resilient portfolios.

Although equity market volatility is likely to increase given more expensive valuations, late cycle dynamics and geopolitical uncertainty, structurally higher nominal growth driven by government spending and technological innovation provides opportunities. Equities remain a great inflation-busting asset class.

In my 30-year investment career, there hasn't been one day where investing felt easy. Our job is to manage risk and uncertainty. When confronting different risks every day, investment processes establish accountability and a shared language. They build an approach which eliminates coordination uncertainty in the face of volatile and emotional markets.

Resilience is a team game and so we must ensure that our investment teams are stable and cohesive so that we may manage our psychology as we navigate troubled waters.

Equities (+) +

We began the year with a constructive view on equities, supported by resilient US growth, a stable labour market and expectations of continued growth in earnings. With the risk of a recession appearing to remain low and inflation relatively contained, the macro backdrop was considered to be supportive for risk assets, even though valuations appeared increasingly stretched.

As the quarter progressed, uncertainty increased. Rising tariff pressures, signs of softer labour data and growing fiscal and political risks began to challenge the outlook. More recently, the escalation of conflict in the Middle East and disruption to energy markets have reinforced the shift towards a more volatile and inflation-prone scenario.

However, stepping back from short-term noise, we retain our conviction in equities. Structurally higher nominal growth, driven by fiscal expansion and technological innovation, continues to support earnings. While volatility is likely to remain high in the near term, equities remain one of the most effective ways to protect against inflation over the medium term.

Government bonds (-) -

We began the quarter with a negative view on government bonds, acknowledging that valuations appeared less stretched as yields had drifted higher, but remaining cautious given persistent concerns around fiscal sustainability and inflation risks.

As the quarter evolved, stronger than expected growth and resilient labour markets led us to question the extent of rate cuts priced by markets. At the same time, fiscal expansion and uncertainty around central bank policy - particularly in the US - reinforced the risk of a more inflationary backdrop.

The conflict in the Middle East has further amplified these risks through higher and more volatile energy prices. Before the crisis started, central banks, particularly the Federal Reserve, were facing pressures to balance signs of labour market softening against inflation risks, potentially leading to more accommodative policy than inflation dynamics would otherwise justify. However, given the risk of energy prices now driving inflation higher, we expect the Federal Reserve to adopt more of a “wait and see” approach and postpone the previously anticipated rate cuts.

In this environment, bonds are less effective as shock absorbers than in the past. We therefore maintain a negative view on government bonds, reflecting an unfavourable risk-return profile and the risk that inflation remains under-estimated.

Commodities (+) 0

We entered the year with a positive view on commodities, supported by tight supply conditions and the strategic role of commodities, particularly gold, as a hedge against geopolitical and fiscal risks.

As inflation risks have increased and the global economy has shifted towards a more volatile, supply-constrained regime, the case for real assets has strengthened. Commodities provide an important hedge against both geopolitical shocks and structurally higher inflation.

However, following the sharp rise in oil prices linked to Middle East tensions, we have moved to a more neutral stance overall. Commodity markets now reflect a more balanced risk-reward profile given uncertainty around both demand and the duration of supply disruptions.

Credit (0) -

We maintained a broadly neutral stance on credit for much of the quarter. The macroeconomic backdrop remained supportive, with resilient growth, solid corporate fundamentals and healthy balance sheets underpinning the asset class.

However, valuations remained a persistent concern. Tight spreads and elevated issuance have left little room for error, particularly in an environment where inflation risks and policy uncertainty were rising.

By the end of the quarter, we had turned more cautious. The combination of tighter financial conditions, potential spillovers from private credit stress and increasing stagflationary risks, particularly following the energy shock, led us to downgrade our view.

Over the past year, we have consistently emphasised one theme: how to build portfolios capable of withstanding a more volatile global environment shaped by geopolitical tensions and a changing world order, technological disruption, the energy transition and demographic divergence.

Recent developments have reinforced this message. The escalation of hostilities in Iran and across the Middle East, and related spikes and volatility in oil prices, have injected fresh uncertainty into an already fragile global outlook. While the full economic fallout remains unclear, events have demonstrated how quickly disruptions can wrong-foot traditional portfolio allocations.

For long-term investors, this underscores the importance of true resilience. This is not merely about preserving capital during brief periods of stress, but constructing portfolios able to generate attractive returns over time despite persistent macroeconomic challenges caused by powerful external forces.

Why private markets – and why now

In this context, private markets have rarely looked more relevant. They offer structural portfolio management advantages over public markets that are especially key during periods of volatility, alongside a recent cyclical decoupling. Taken together, they represent a compelling portfolio allocation both in the current environment and longer term.

Structurally, private investments are less exposed to the sentiment swings of public indices. Closed-ended fund structures provide locked-in capital, enabling managers to deploy capital opportunistically during downturns and time portfolio exits more effectively, avoiding forced sales.

Private markets are also more specialised, accessing a broader opportunity set. Managers can target segments with balanced capital supply and demand due to barriers to entry, invest in domestically focused companies that are less exposed to global shocks, and access assets with differentiated risk exposures and lower correlation to listed markets.

Cyclically, many private market segments — corporate private debt being a notable exception — have experienced four years of subdued fundraising, investment, valuations and exits, even as public equities reached record highs and credit spreads tightened. Combined with private capital concentration in larger funds and transactions, this has created attractive entry points and inefficiencies in other parts of the market, which can translate into compelling return opportunities.

Not all private market strategies are equally resilient

While private markets as a whole offer structural advantages, the degree of resilience varies significantly across and within asset classes.

- In private equity, small and mid-sized buyouts and continuation vehicles have proven more resilient than large buyouts.

- In venture, early-stage opportunities retain their fundamental appeal while late-stage AI investments carry unprecedented valuation and concentration risk.

- In private debt, scrutiny regarding direct lending contrasts with the structural soundness of the wider private debt and credit alternatives universe.

- In real estate, the gap between prime and commodity assets has never been wider.

- In infrastructure, operational assets with contracted revenues are gaining scarcity value while development-stage projects face headwinds.

This is not a new observation. As readers of our previous outlooks will recognise, our focus on structurally resilient segments – smaller and mid-market strategies, operational value creation, diversified credit alternatives and essential-service assets – has been a consistent theme. The current environment has validated, rather than prompted, this positioning.

Private equity: the end of bigger is better

Private equity fundraising remains muted, supporting attractive entry points. Investment and exit activity have recovered modestly from the lows of early 2025, though the fallout from the Iran conflict may delay a broader recovery and the exit backlog continues.

We continue to see the most compelling opportunities among smaller companies. Depending on definitions and data sources, small and mid-sized buyouts benefit from persistent valuation discounts of 20–40% relative to large buyouts – with the widest discounts at the small end of the market – while offering exposure to businesses less tethered to global markets, with greater transformational growth potential. Over the past four years, small buyouts have outperformed mid, and mid buyouts have outperformed large, supporting the view that entry discounts translate into better net return potential.

Continuation vehicles, which reached record transaction levels in 2025, are gradually and partially substituting sponsor-to-sponsor transactions (secondary buyouts), which had become the dominant deal source for large-cap funds. Critically, our research shows that over 80% of the growth in continuation investments is structural rather than cyclical. This is driven by continuation structures offering inherent advantages over traditional buyouts: lower fees, faster liquidity and more predictable return profiles with tighter dispersion.

In venture, the divergence between stages mirrors the pattern we observe across private markets more broadly. Early-stage markets offer selective and compelling opportunities globally, underpinned by multi-polar innovation at reasonable valuations. By contrast, late-stage funding rounds (Series D+) present significant concentration risk: AI now dominates deal value and valuations have surpassed 2021 peaks. We are cautious on this part of the market, given how prior technology cycles have played out.

Private debt and credit alternatives: look for diversifying and diversified

There is quite a lot of noise in headlines around private debt. Traditional direct lending faces increased scrutiny over sector concentration – particularly in areas with risks of AI disruption, such as software – as well as redemption pressures for certain private debt funds. Importantly, the gating mechanisms embedded in these funds minimise the risk of forced selling in the corporate loan market more broadly.

The need for stable yield, income and return continues to persist. We see attractive opportunities across a wide universe of credit strategies that offers attractive diversification through collateral- and contract-backed strategies, with differentiated and resilient risk profiles.

Infrastructure debt, with its structural need for capital and collateral-based investments, offers one such opportunity. Commercial real estate debt is supported by properties that have already seen a reset of its valuations and so offers a lower-basis entry point. Asset-based finance (ABF) focuses on investments in large numbers of debt contracts with a diverse obligor base and the backing of everyday things like homes, cars and airplanes. It also offers a floating-rate exposure, which is beneficial in an environment where interest rates may rise. Lastly, insurance-linked securities offer macroeconomic decorrelation in a world with more geopolitical risk.

Infrastructure: energy transition tailwinds remain

Energy security remains a key theme supporting renewables build-out globally, and infrastructure is one of the areas where the structural advantages of private capital – long-duration commitment, operational engagement and locked-in capital – are most evident.

The Iran conflict further reinforces the strategic case for the energy transition, though acceleration is likely to be policy-driven, geographically uneven, and to materialise over time. In the near term, operational renewables benefit directly from higher power prices.

Valuations have also reset meaningfully following the interest rate cycle, with US policy changes, UK regulatory adjustments and revised long-term assumptions creating attractive entry points. Additionally, surging power demand driven by AI and data centre expansion is creating a structural demand catalyst for renewable generation capacity and grid infrastructure.

Europe and Asia remain central to future renewable expansion, while US dynamics have become more complex following policy changes. Across all geographies, renewables remain the cheapest source of new-build generation, and battery storage has emerged as a particularly compelling sub-sector.

Real estate: at an inflection point

We previously highlighted expectations of a real estate recovery, with current vintages positioned attractively. Recent quarterly data supports this view, with a nascent rebound in transaction activity and pricing, albeit highly uneven across sectors, geographies and asset quality tiers. The recovery has been predominantly income-driven, with capital appreciation still modest, and the gap between best-in-class and average assets has never been wider.

The Iran conflict, and a related potential resurgence in inflation and resulting rate implications, has the potential to stall this. However, constrained supply continues to support rental income, particularly for prime assets, with construction costs under further upwards pressure from supply chain disruption. Properties providing indirect inflation protection through shorter-term contracts, such as self-storage, or contractual inflation pass-through will provide effective near-term real cashflow protection.

Operational expertise, asset enhancement and sustainability improvements are increasingly critical to long-term value creation. Additionally, a substantial volume of maturing commercial real estate debt – further complicated by the current rate environment – is catalysing compelling recapitalisation and secondaries opportunities.

Sustainable investment is entering a new phase. After years of rapid growth, a backlash began two to three years ago: political headwinds in the US, questions about greenwashing in Europe, and persistent concerns that incorporating sustainability considerations comes at a cost to returns. Global sustainable fund flows turned negative in several quarters during 2024-25[1].

The critics have a point that demands an honest response. Not every social or environmental challenge translates into a compelling investment case. For example, antimicrobial resistance costs the global economy an estimated $1 trillion to $3 trillion per decade, yet the investment returns available today to address it are low. Air quality and weak pollution controls affect 6.7 billion people, but the investable market is small and slow-growing. Unfortunately, social urgency does not equate with investment opportunity.

A slowdown in policy action makes this distinction more important. The regulatory frameworks that convert social costs into financial signals — climate regulation, mandatory disclosure, environmental liability — have stalled or reversed in several major economies. Without policy catalysts, many socially important themes remain financially uninvestable at the scale they need. We expect the current stalling will prove temporary; growing environmental challenges and intensifying social tensions will inevitably demand a policy response. However, for investors navigating this environment, clarity about where the financial case genuinely holds is both a prerequisite and an opportunity to look through headlines to the underlying fundamentals.

The good news is that the overlap between investment attractiveness and social importance is far larger than the current narrative suggests. We have developed a dual-materiality framework that scores 55 global themes independently on two dimensions: investment attractiveness (based on market size, growth rate, expected returns, technology readiness and market maturity) and social importance (based on directly affected populations, the economic cost of inaction, alignment with Sustainable Development Goals, employment impact and investment scale required). Each input measure is normalised to a 1-10 scale using a consistent methodology[2] so that themes can be compared on a like-for-like basis.

This is a blunt, top-down exercise which cannot replace thorough bottom-up analysis but demonstrates that trade-offs exist and provides a framework to identify the most attractive areas of focus.

Themes representing over 40% of the total market opportunity of the themes plotted score above the median on both dimensions, where strong financial returns and significant societal benefit coexist. These include AI and advanced computing (the highest combined score in this dataset), the clean energy transition (a $1.8 trillion clean technology market growing at 13% annually), digital infrastructure and inclusion, biodiversity and natural capital, and carbon markets. Collectively, these represent some of the deepest and fastest-growing capital pools in the global economy.

Source: Schroders, March 2026

Other themes – collectively less than 15% of the total opportunities plotted – offer high social importance but below-median investment scores. These include water security and fertility decline. These trends reflect unavoidable, intensifying structural trends for which their financial impacts are already being felt and will grow in the future, likely prompting the policy attention which could strengthen their financial impacts.

Across Schroders, our focus is on the themes and trends where we believe the investment consequences are strongest, now or in the future, and where we are best placed to develop insights, analysis and investment tools to support our clients. Examples include biodiversity and natural capital, as well as climate transition and clean energy. We recognise that many investors prioritise social and environmental objectives, as well investment returns, and we have developed tools, solutions and investment strategies to support them, armed with an understanding of trade-offs and mitigants.

Our view of investment risk and opportunity underpins our firmwide commitment to sustainability. Structural trends in society, the environment, global economy, industries, and portfolios demand new perspectives and approaches. By maintaining rigour over the investment opportunities sustainability-related themes present, we can support better investment decisions and help play a role in supporting policymakers to unlock change where it is needed.

[1] Source: Morningstar, "Global Sustainable Fund Flows: Q4 2025 in Review", February 2026

[2] Log-transformed where data is heavily skewed, winsorised to prevent outlier distortion, and linearly scaled from 1 to 10

Source: Schroders Economics Group, February 2026

Baseline: We continue to forecast global growth to be stronger than is generally expected, providing a supportive backdrop for risk assets. But with some central banks set to seize on one-off declines in inflation to cut interest rates further and keep monetary conditions loose, we remain concerned that running growth hot will ultimately lead to elevated inflation down the track. Such risks may drive long-term interest rates higher, causing more bouts of market volatility and exposing fragile sovereign debt dynamics once again. We see global GDP growth at 2.9% for 2026 and 2.7% for 2027; global inflation (CPI) at 2.4% for 2025 and 2.4% for 2026; and US interest rates at 3.25% at end-2025 and 3.25% at end-2027.

Mid-term push: In a desperate push to boost poll numbers the US administration delivers additional fiscal stimulus, introduce price controls, push down credit card and mortgage borrowing costs and lean on the Fed to cut policy rates. The subsequent overheating of the US economy eventually forces the Fed to reverse course in 2027, while the spillover prompts other central banks to raise rates.

Global fiscal crisis: A global fiscal crisis emerges in Q3 2026 as investors lose confidence in debt sustainability, prompting bond‑market vigilantes to demand higher yields. Sovereign borrowing costs rise sharply, tightening financial conditions and forcing governments to scale back spending. The resulting drag on demand leads to weaker growth and falling inflation.

Second wave inflation: Inflation rises globally due to a combination of supply-side shocks such as higher trade tariffs and a renewed surge in food and energy inflation. Tight labour markets lead to second-round effects and cause higher inflation to become ingrained. As a result, central banks raise interest rates which, in addition to a squeeze on real incomes, causes growth to be weaker than in our baseline forecast.

AI boom: Rapid adoption of AI results in a period of robust, investment-led economic growth that boosts productivity, but widespread automation begins to displace workers, lifting unemployment and weighing on consumer spending. The AI boom creates some supply‑chain and energy‑related price pressures, but these are outweighed by productivity gains and weaker consumption that gives central banks room to cut rates.

AI bust: An AI bubble in the global equity market bursts in Q3 as it becomes clear that the sector cannot deliver on lofty expectations. Capex spending reverses, and consumer spending weakens as a mild recession causes unemployment to rise while tumbling stock markets hit sentiment. Meanwhile, weaker growth eases inflation pressures and allows central banks to lower interest rates that eventually generates a consumer-led cyclical recovery.

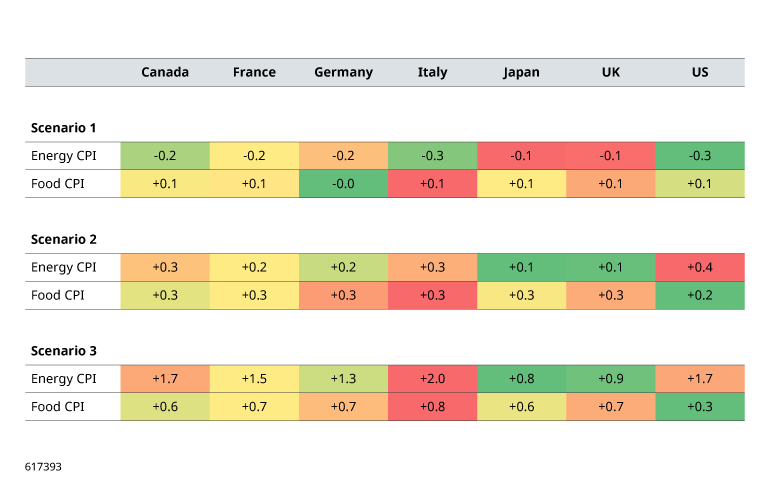

Iran conflict – the impact on inflation

At the time of writing, oil prices are at troublesome levels; it is now just a question of how high and for how long. To understand how this could affect inflation outcomes in the G7, we have modelled three scenarios and compare this to a counterfactual that the conflict never begun. The three scenarios are as follows:

- Scenario 1: A quick resolution, in which the price of Brent crude reaches $100/bbl but then falls back quickly below the counterfactual. Inflation ends up being lower for most economies given that food and energy prices end up lower than they would in the counterfactual, compounded by the dollar being weaker in relative terms.

- Scenario 2: A stalemate scenario in which the price of Brent crude remains at $100/bbl for six months before gradually normalising. Inflation is around half a percent higher than it otherwise would have been.

- Scenario 3: A worst-case scenario in which the price of Brent crude climbs to $150/bbl and remains there as the Strait of Hormuz remains disrupted for a long time. Inflation would be considerably higher in this scenario.

Source: Schroders Economics Group, 24 March 2026

Subscribe to our Insights

Visit our preference center, where you can choose which Schroders Insights you would like to receive.

Autheurs

Topics