How European corporate profits powered ahead in Q1

We look at what was behind a strong first quarter for eurozone earnings and what lies ahead, with fund manager Martin Skanberg.

Authors

European companies were always likely to post strong year-on-year (y/y) earnings growth in Q1 2021. They faced, after all, a soft comparative quarter in the Covid-disrupted Q1 2020. While 2020 started fairly normally, Covid restrictions began to be imposed from February in some European countries. This saw demand fall sharply with some industries closed down entirely while other businesses had little time to adapt to new ways of working.

But the strength of earnings growth in Q1 2021 is still striking. European companies on average reported earnings growth of 95.4% y/y, according to data from Refinitiv (based on 306 companies in the Stoxx 600 index).

European Equities fund manager Martin Skanberg said: “Earnings growth has been particularly strong in sectors sensitive to the economic cycle: industrials, banks and – above all – consumer cyclicals.”

The consumer cyclicals sector is made up of companies sensitive to economic conditions – such as carmakers and retailers – many of whom saw demand fall sharply in Q1 last year. Such companies are, however, well placed to benefit from the re-opening of economies this year.

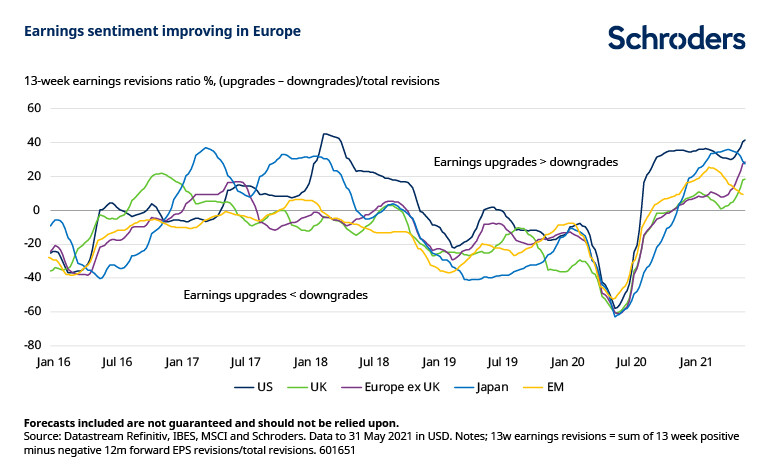

The strong reporting season has seen analysts start to rapidly upgrade their earnings forecasts in recent weeks. The sharp upward lines – purple for Europe ex UK and green for UK – indicate growing positive momentum with the number of upgrades to earnings estimates outpacing downgrades.

The strong Q1 earnings growth is expected to be followed by a similarly strong Q2.

Martin Skanberg said: “For many sectors, both volumes and pricing are recovering at the same time. Supply constraints in some sectors are also helping to lift prices and feeding through to higher profits. Cost control is another element helping to support profits.

“The second quarter looks set to be another very positive quarter for corporate earnings as the recovery from the pandemic continues. Thereafter, we will see some moderation in earnings growth and of course Q1 next year will face a difficult comparator quarter.”

The strength of earnings in Q1 contrasts with the somewhat gloomy sentiment towards Europe that prevailed during the quarter, due to its slower vaccine roll-out relative to the UK and US. However, eurozone shares (as represented by the MSCI EMU index) have been some of the strongest performers year-to-date, returning 14.1% in comparison to the MSCI World’s 11.5% (both in euro terms and as at 31 May).

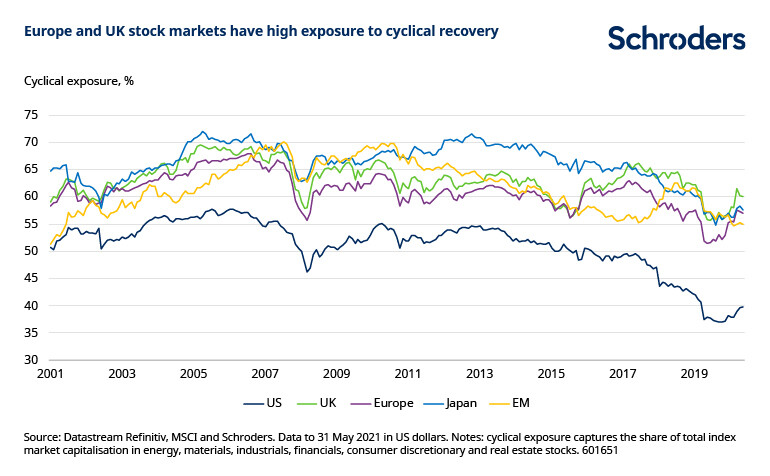

But in many ways it shouldn’t be surprising to see European stock markets perform well this year. Lengthy lockdowns weighed on business activity for much of last year, meaning there was greater scope for a rebound when the recovery started to come through. And Europe has relatively high exposure to those cyclical sectors (such as industrials) which tend to benefit the most when the economic cycle starts to turn more positive.

Martin Skanberg said: “The good recent performance of Europe compared to other regions shows the importance of remaining invested and not being swayed by short-term newsflow. Stimulus is still coming through from governments and central banks which should continue to support equities.

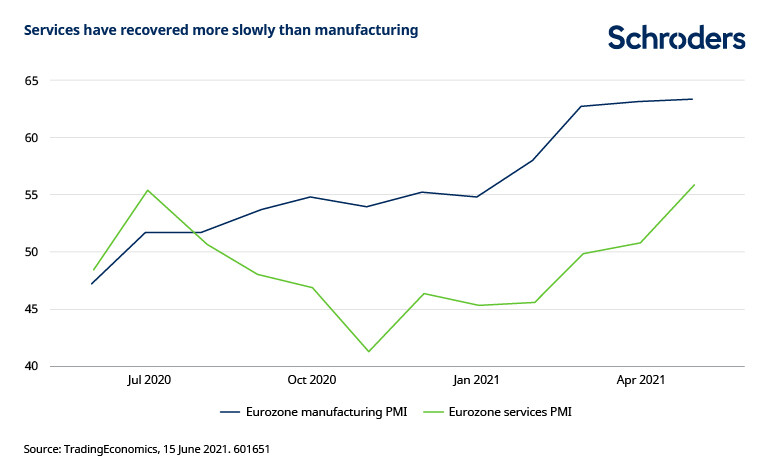

“Manufacturing indicators are at record highs, as seen in the chart below. We will need to watch though for any signs of slowdown in China, which is further ahead in terms of recovering from the pandemic. A slowdown in China could lead to the manufacturing sector decelerating in Europe.

“However, services have been much slower to recover, with the services PMI still below the 50 mark as recently as March. As European countries continue to ease Covid restrictions and economic activity normalises, there is an opportunity for the services sector to play catch-up. Companies in those sectors could potentially then take over market leadership from the manufacturing-related firms that have largely driven the recovery so far.”

The PMI is an index of business activity based on a survey of private companies in the manufacturing and services sectors. A reading above 50 denotes expansion while below 50 denotes contraction.

Zapisz się na nasze Analizy

Odwiedź nasze centrum preferencji, gdzie możesz wybrać, które Analizy przygotowane przez Schroders chcesz otrzymywać.

Authors

Tematy